LIVINGSTON, Tenn. — Three family-owned companies here collected a combined $1,730,503 in Paycheck Protection Program loans — and later had $1,741,511 forgiven with interest — according to federal PPP records reviewed by this newsroom. Within months of those forgiveness decisions, the family commissioned a multi-million-dollar custom houseboat, a conspicuous purchase that has fueled community questions about whether pandemic relief meant for workers actually protected paychecks.

The businesses span very different lines of work: Cooper Recycling (recyclable material wholesaling), The Steel Coop (full-service restaurant), Hwy 111 Station & Deli (convenience/restaurant), and Hwy Tire (tire shop). Each, with the exception of Hwy Tire, took a first-draw loan in spring 2020 from FirstBank and a second-draw loan in early 2021 from Itria Ventures LLC, a fintech lender. All seven loans were forgiven.

The numbers they swore to

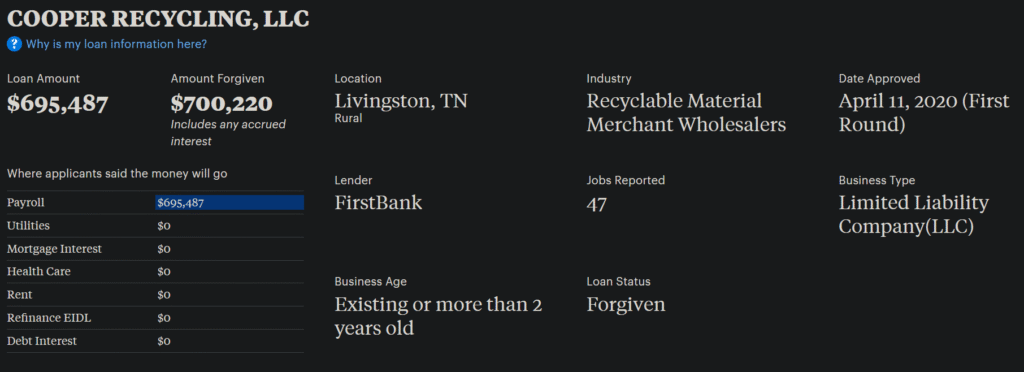

- Cooper Recycling reported 47 jobs on its first draw ($695,487) and 56 on the second ($539,327).

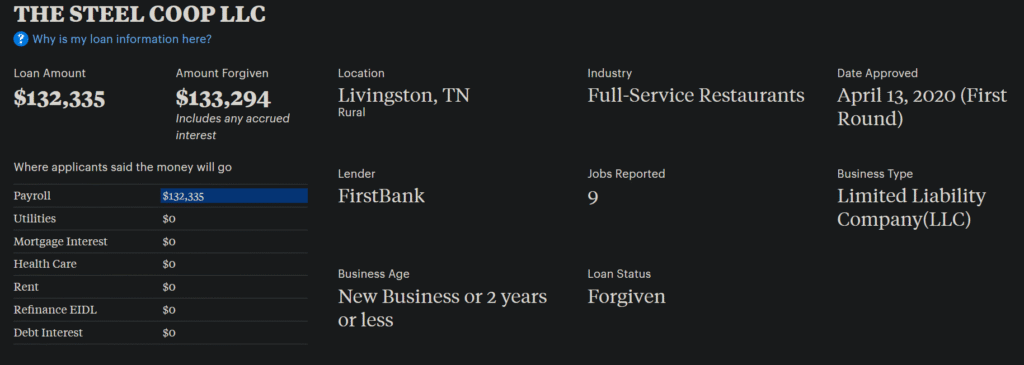

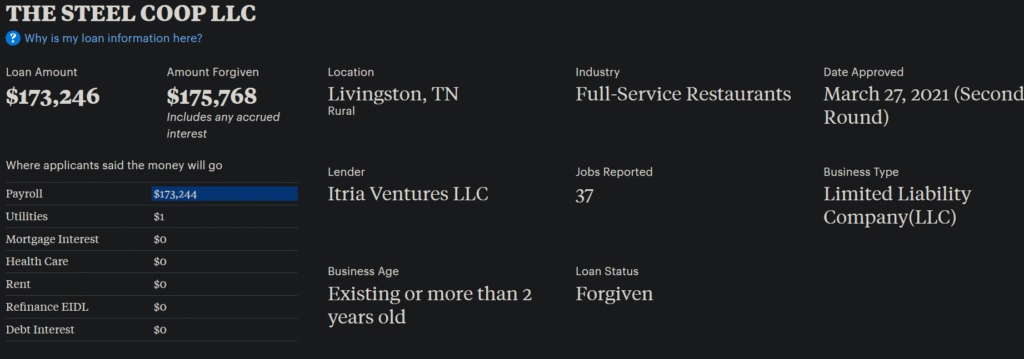

Approx. dollars per reported job: $14,798 (first), $9,631 (second). - The Steel Coop reported 9 jobs on its first draw ($132,335) and a striking 37 jobs on the second ($173,246).

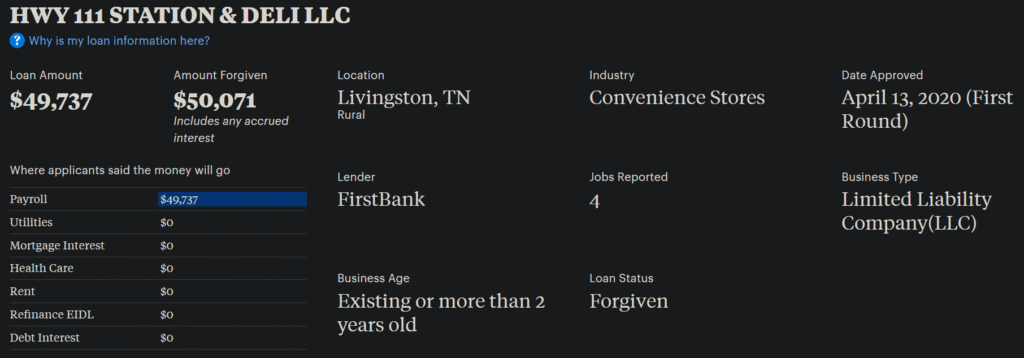

Approx. dollars per reported job: $14,704 (first), $4,682 (second). - Hwy 111 Station & Deli reported 4 jobs on its first draw ($49,737) and 10 on the second ($84,522).

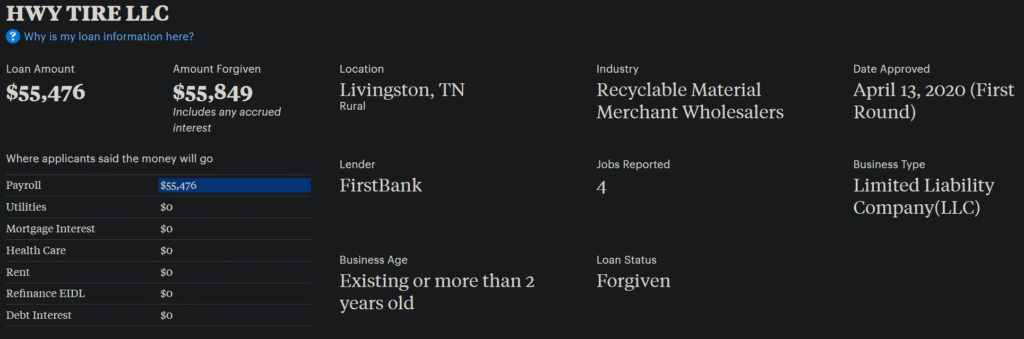

Approx. dollars per reported job: $12,434 (first), $8,452 (second). - Hwy Tire reported 4 jobs on its first draw ($55,849) Approx. dollars per reported job: $13,962. There was no second draw indicated.

On paper, nearly every dollar was earmarked to payroll; the second-draw filings show a token $1 for utilities — a quirk sometimes seen in automated lender forms. All seven loans reached full forgiveness (forgiveness totals exceed principal because PPP also forgave accrued interest).

Why this matters

PPP wasn’t free money for expansion or big-ticket toys; it was an emergency program to keep workers on payroll. To earn second-draw money in 2021, companies had to certify a 25% or greater drop in gross receipts in any 2020 quarter compared with 2019. For restaurants, that’s plausible during shutdowns; for essential recyclers or convenience operations, it depends on the books. Either way, those claims should be backed by quarterly P&Ls and bank-verified payroll.

What doesn’t add up — yet

- Headcount spike at The Steel Coop. Going from 9 to 37 reported jobs during the pandemic is unusual for a rural full-service restaurant. Maybe they ramped up seasonal or part-time work, added catering, or reopened with large staff. Or the figure could be inflated. Only payroll registers, IRS 941s, and state unemployment reports can resolve that.

- Second-draw eligibility across all three entities. Each company had to meet the 25% revenue-drop test for the second draw. If any did not, forgiveness should not have been automatic. The quarter-over-quarter math is checkable.

- The optics problem. Commissioning a ~$2 million custom houseboat soon after forgiveness doesn’t prove misuse — owners can spend personal funds however they wish — but the timing invites scrutiny. The key question is whether PPP dollars truly flowed to eligible payroll during the covered periods, not to owners via draws or to unrelated capital projects.

Questions the companies should answer — with documents

- Payroll: Provide full payroll registers by pay period, IRS Form 941s, state UI wage reports, and bank statements for the covered periods of each loan. Do the cash outflows match the PPP proceeds?

- Second-draw test: Identify the 2020 quarter(s) used to claim the ≥25% drop, and release P&Ls and sales-tax filings supporting the calculation.

- Headcount methodology: Explain the Steel Coop’s jump to 37. Were these FTEs, part-timers, temporary hires, or counts across multiple locations?

- No double-counting: If employees rotated among commonly owned entities, how did the companies prevent duplicate wage claims in forgiveness?

- Use of funds: Did any PPP-covered dollars directly or indirectly fund owner distributions or capital purchases? Share reconciliations.

- Lender oversight: What did Itria Ventures and FirstBank review for forgiveness, and what documentation did the companies submit?

What we know — and what we don’t

We know the dollar amounts, the reported jobs, the lenders, and that all seven loans were forgiven with interest. We don’t yet know whether the bookkeeping and bank trails confirm those headcount and revenue claims — or whether some of the payroll story collapses when tested.

The standard of proof

This is not a conviction in the court of public opinion. It is a demand for receipts proportional to the $1.74 million these businesses received and the public purpose those dollars were meant to serve. If the paperwork is clean, the owners can end the speculation by releasing it. If it isn’t, the SBA OIG and DOJ’s COVID-19 Fraud Task Force have well-worn playbooks for claw backs and prosecutions.

Have documents, tips, or first-hand knowledge about payroll or revenue at these companies during 2020–2021? Let us know TIPS@UCExaminer.com.

{kind=link}

They also received over 140k for cooper farms, somehow

Thorough investigation and excellent reporting! Great job!

The Coopers are GREAT PEOPLE They are great businessmen They did NOT invent PPL They would have been idiots to have NOT taken advantage of it I compare it to taking a lawful tax deduction What they did with the money they saved is none of my damned buisness Guess it’s none of your either😂

Actually it is our business, it was our tax payer dollars… If they used the loans as intended strictly for payroll purposes then sure everything is above board, but if that’s not the case the need to be investigated. I don’t care what kind of people they are, if they did misuse federal disaster money for personal gain they deserve to be held accountable. And the fact that during the time and after the loans for payroll were taken and forgiven they settled a federal class action lawsuit for wage theft then bought a 2 million dollar boat… The timing and the fact that they already were doing shady payroll stuff invites more scrutiny…

Doesn’t pass the smell test. Unfortunately our government regulator have no interest in doing their jobs as oversight for these “free money” programs. Afterall, it’s OPM.